Popular Articles

“From Surviving to Thriving: A Modern Guide to Financial Freedom in 2025”

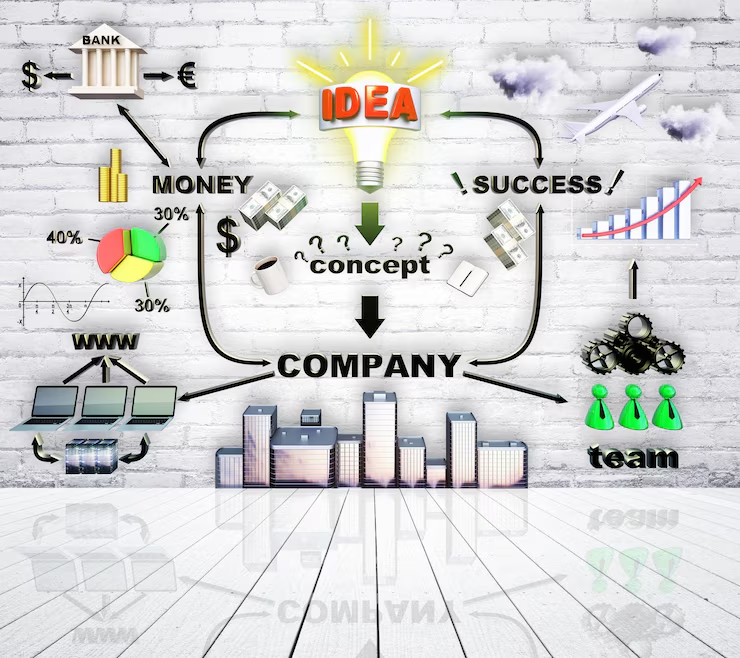

🧭 Introduction: It’s Not About Being Rich — It’s About Being Free Have you ever felt like you’re working just to pay bills? That moment when your salary hits the bank… and then disappears into rent, EMIs, UPI payments, Swiggy orders, and credit card bills? You're not alone. But here’s the truth: Financial freedom is not about having crores. It’s about having control. Control over your time. Your decisions. Your life. Let’s walk you through a realistic, action-driven guide to go from financial survival to financial freedom — no matter your income level. 🌱 Step 1: Define Your “Why” — Your Money Vision Before any money plan, define your why. Ask yourself: Why do I want to save money? What does freedom mean to me? What would I do if I didn’t have to worry about money? Examples: Travel the world in 5 years 🌍 Be debt-free in 12 months 💳 Start my own business 🏢 Support my parents 👪 📌 Write this down. Stick it on your wall. This is your fuel. 💼 Step 2: Pay Yourself First Before you pay bills or spend on others, pay yourself. “Savings is not what’s left after spending. It’s the first thing you do.” Set up auto-debit or SIP on your salary day. Even if it’s ₹500/month — it’s a start. 📊 Step 3: Build a One-Page Budget Most people quit budgeting because it feels complicated. Let’s simplify: Your One-Page Budget: 💡 Essentials – 50% 🎉 Lifestyle – 25% 💰 Wealth – 15% 🚨 Emergency – 10% Use a Google Sheet or apps like GoodBudget, ET Money, or Wallet. 💣 Step 4: Break Up With Bad Debt Credit card interest in India = 36–42% per year. That’s not just debt — that’s theft. How to Fix It: Stop using credit for wants Pay more than the minimum due Consolidate loans if possible Sell something, freelance, reduce spending — kill it fast 💥 Freedom starts where debt ends. 🏥 Step 5: Don’t Skip Insurance (It’s Not Boring — It’s Smart) Many people in their 20s and 30s avoid insurance. But one hospital bill can destroy years of savings. You need: ✅ Health Insurance (₹5–10L cover) ✅ Term Life Insurance (if you have dependents) ❌ Skip ULIPs, endowment, traditional LIC plans (low ROI)

🏦 USA Bank Loans in 2025: Navigating the Future of Borrowing

Section 1: Who’s Borrowing and Why? The profile of borrowers in 2025 is diverse and dynamic: Young professionals and millennials account for the largest share of mortgage and personal loan seekers, eager to capitalize on historically moderate interest rates before potential hikes. Gig economy workers and freelancers demand flexible, income-sensitive loan products that accommodate irregular cash flows. Small business owners look for quick, technology-driven access to capital to fuel innovation and expansion. Environmentally conscious consumers gravitate toward green loans rewarding sustainable investments like solar panels, energy-efficient homes, and electric vehicles. Section 2: Emerging Loan Products Transforming the Market 1. AI-Powered Personalized Lending Banks deploy AI algorithms that analyze beyond traditional FICO scores—examining behavioral data, transaction histories, and social signals—to provide tailored loan terms, often with better rates for lower-risk borrowers. 2. Green Financing Options Eco-friendly mortgages, auto loans, and personal loans are increasingly popular, offering reduced interest rates and cashback incentives to promote sustainability goals aligned with national climate initiatives. 3. Flexible, Income-Responsive Repayment Plans These loans adjust monthly payments based on actual income fluctuations, especially beneficial for gig workers and freelancers who face variable earnings. 4. Instant Microloans Leveraging mobile platforms and real-time data, microloans up to a few thousand dollars can be approved within minutes, providing emergency liquidity to underserved segments. Section 3: The Role of Technology in Lending Seamless digital applications enable borrowers to apply for and receive loans from their smartphones in under 10 minutes. Blockchain and smart contracts ensure transparency, reduce fraud, and automate disbursements and repayments. AI chatbots and voice assistants provide personalized guidance, answer queries, and even assist with loan management. Embedded lending integrates loan offers directly into popular apps and marketplaces, enabling frictionless borrowing at the point of need. Section 4: Challenges and Risk Management While innovation expands access, borrowers must be mindful of: Interest rate volatility: With inflationary pressures, fixed-rate loans are often safer bets. Over-indebtedness: Easy digital access can tempt borrowers to take on unsustainable debt loads. Privacy concerns: The growing use of personal data in underwriting demands vigilance about data security. Complex fee structures: Hidden fees, prepayment penalties, and variable rates require thorough review before commitment. Section 5: Practical Tips for Borrowers in 2025 Thoroughly compare loan offers including APR, fees, and repayment flexibility. Maintain or improve your credit profile by timely payments and minimizing credit utilization. Utilize financial apps and AI advisors to simulate repayment scenarios and manage budgets. Explore green loans and incentives if you qualify to reduce overall borrowing costs. Lock in rates early if forecasts suggest rising interest rates. Section 6: Looking Ahead – The Future of Borrowing Voice-activated loan management: Enable hands-free control over payments and queries. Sustainability-linked lending: Borrowers rewarded for reducing carbon footprints and social impact. Real-time financial coaching: AI-powered systems proactively guide borrowers to optimal financial decisions. Integrated ecosystems: One platform to borrow, save, invest, and insure—simplifying financial lives. Conclusion: Empowered Borrowing in a Changing World Bank loans in 2025 offer unparalleled opportunities, fueled by technology and a borrower-centric approach. However, navigating this landscape requires awareness, prudence, and smart use of the tools at your disposal.

🚀 Fueling American Entrepreneurs: How Bank Loans Are Powering Small Businesses in 2025

🏁 Introduction: A New Era for American Hustle In the land of opportunity, 2025 has become a breakthrough year for small business financing in the USA. With over 33 million small businesses contributing to nearly half of the nation’s jobs, American banks have shifted gears — offering faster, fairer, and more flexible loan solutions for dreamers, creators, and risk-takers. This blog dives deep into how modern bank loans are transforming Main Street — not just Wall Street — one espresso bar, Etsy shop, and tech startup at a time. 📊 Section 1: The State of Small Business Lending in 2025 Category 2020 2025 (Now) Avg. Loan Approval Time 3–5 weeks 24–48 hours Avg. Approval Rate (under $100K) 40% 70%+ Digital Application % 20% 95% AI-Involvement in Underwriting 5% 85%+ Loans to Minority-Owned Biz $25B $80B+ 💡 Section 2: What’s Changed for Borrowers? 🔹 1. AI-Powered Risk Analysis Banks now use: POS (point of sale) data Inventory turnover rates Social engagement metrics Customer review sentiment You can qualify for a business loan without traditional collateral or even a long credit history. 🔹 2. Revenue-Based Repayment Instead of fixed EMIs, new loans adjust monthly based on: Your actual sales Seasonality of your business Cash flow projections Perfect for restaurants, salons, creators, and service businesses. 🔹 3. Loan + Growth Packages Many banks offer bundled support: Business coaching Web hosting credits Financial literacy tools Exclusive advertising grants 💰 Section 3: Most Popular Small Business Loans in 2025 Loan Type Avg. Amount Who It’s For Benefits Microloans $10K–$50K Creators, solopreneurs Fast approval, minimal docs SBA-Backed Green Loans $50K–$350K Eco-conscious businesses Subsidized interest, tax breaks Revenue-Share Loans $25K–$150K Retail, eCom, seasonal businesses Pay as you earn Minority Biz Loans $30K–$250K BIPOC, Women, Veteran-owned startups No-collateral + mentoring support Equipment Financing $15K–$500K Manufacturing, logistics, clinics Lease-to-own, 100% financed options 🧠 Section 4: Smart Tips for 2025 Borrowers ✅ Build Digital Creditworthiness Include data from payment apps (like Stripe, PayPal, Square) to strengthen your loan profile. ✅ Use Open Banking Tools Apps like Brex, Lendio, and QuickBooks Capital allow smart loan comparison with real-time cashflow analysis. ✅ Negotiate Even AI-Set Terms Most platforms still allow you to request human review — and get better terms. ✅ Monitor Your “Lending Health Score” Banks are now showing borrowers personalized risk profiles — track this monthly. ⚠️ Section 5: Pitfalls to Avoid ❌ Taking stacked loans from multiple lenders (can lead to cashflow chaos) ❌ Ignoring fine print in BNPL-style business credit ❌ Choosing loans with prepayment penalties ❌ Over-relying on automated approvals without business planning 🧭 Final Thoughts: The Best Time to Grow is Now “The most successful business owners in 2025 aren’t those with the biggest teams — they’re the ones who borrow smarter.” Bank loans have become more democratic than ever. Whether you’re selling on Shopify or opening a local bakery, the system is finally designed to fund ambition, not punish risk. If you're thinking of scaling, pivoting, or launching your dream — the tools, money, and technology are ready. Are you?

🇺🇸 How Bank Loans Are Reshaping the American Dream in 2025

🏠 Introduction: The New Face of the American Dream For generations, the American Dream meant owning a home, building a business, or putting your child through college. But in 2025, how Americans pursue and fund that dream has fundamentally changed — and the key driver? Bank loans. Today’s loans aren’t just financial tools. They’re empowerment engines backed by AI, personalized data, and inclusive policies. This blog dives into how U.S. bank loans in 2025 are redefining access, opportunity, and the modern American lifestyle. 💳 Section 1: Loans Are Smarter, Not Just Faster 🧠 Powered by AI Loan applications now take minutes, not weeks — thanks to: AI-driven approval systems Real-time credit scoring Predictive income analysis Banks use behavioral finance tools to tailor loans to your lifestyle, not just your paycheck. 📡 Embedded Everywhere From your shopping cart to your mobile wallet: Auto loans offered via car apps Buy Now Pay Later loans now bundled with insurance Home renovation loans triggered by smart-home platforms 🧱 Section 2: Building the New American Dream 🏘️ 1. First-Time Homebuyers Win Big 2025 programs offer subsidized interest for under-35 buyers Virtual property tours + instant digital mortgage approval Green homes? Lower rates and tax deductions 👩💼 2. Business Loans = Startup Fuel Flexible repayment based on real-time sales Minority-owned startups receive faster underwriting Local banks now partner with fintechs to issue AI-backed microloans 🎓 3. Education Loans Go Human Loans tied to future income potential, not family assets Deferred payments until after skill-based employment begins Incentives for graduates who choose public service or sustainability jobs 📈 Section 3: U.S. Loan Stats in 2025 Loan Type Avg. Approval Time Avg. Interest Rate Notable Trend Personal Loans 3 minutes 6.9% Used for consolidating BNPL debt Home Loans 24 hours 4.5% Eco-upgrades lower rates Auto Loans (EV only) Instant 2.1% Heavily subsidized Student Skill Loans 10 minutes 0–5% Outcome-based pricing Business Loans 1–2 days 7.5% Revenue-tied repayments 🧭 Section 4: Navigating the Pitfalls As loans get smarter, so do the risks: Loan stacking from multiple apps can go unnoticed until it’s too late. Algorithm bias still exists — leading to unfair rates in some communities. Data overload can overwhelm borrowers who don’t understand what’s being tracked. “Zero interest” deals may hide fees or inflate item prices. 🔒 Pro Tip: Always use a trusted personal finance app to monitor your total borrowing and terms — tools like Truebill, Rocket Money, or YNAB help track everything in real time. 🧠 Section 5: Borrow Better — 2025 Rules for Smart Loans Check the Total Loan Cost, not just the EMI. Negotiate the AI Offer — many banks allow manual override requests. Look for Green Perks — eco-conscious behavior = lower rates. Ask for a Human Review if you get denied — you might get a better deal. Know When to Say No — pre-approved doesn’t mean pre-needed. 🔮 Conclusion: Loans as Leverage, Not Chains “The new American Dream isn’t built on waiting — it’s built on wisely leveraging opportunity.” In 2025, loans aren’t just about survival — they’re tools for growth, freedom, and acceleration. Used wisely, today’s loans can help you build your future without burying your present.

🏛️ From Paper to Pixels: How Bank Loans in the USA Have Entered the Future (2025 Edition)

🌐 Introduction: The Digital Loan Boom in America In 2025, walking into a bank to get a loan feels as old-fashioned as using a fax machine. Banking in the USA has fully embraced the fintech frontier — and bank loans have become faster, smarter, and far more user-centric. If you're thinking of applying for a loan today, you're entering a world of data-driven decisions, zero paperwork, and real-time approvals — all in the palm of your hand. 🔍 Section 1: Key Trends Defining Bank Loans in 2025 1. Hyper-Personalized Lending Loan offers are now based on: Your online purchase habits Social signals Gig and side-hustle income AI-inferred life events (e.g. planning to get married? You might get a home loan offer automatically) 2. No-Touch Loan Applications Thanks to biometrics and open banking, you can: Apply via voice or fingerprint Get approved in under 5 minutes Track everything in a single mobile dashboard 3. Green is the New Gold Sustainability scores now influence loan interest rates. Choosing an eco-home or electric vehicle? Expect: Government-backed low-interest loans Eco-incentives from banks Credit boosts for green behavior 📊 Section 2: How Different Americans Are Using Loans in 2025 Borrower Type Most Popular Loans Features Borrowers Love Young Professionals Student loan refinancing, EV loans Fast mobile approvals, tax-linked repayment Entrepreneurs Business expansion loans Revenue-based repayment, startup accelerator ties Remote Workers Relocation/home loans Geolocation-based pre-approval Parents Education and home improvement loans Flexible EMIs, kid-focused perks 💬 Section 3: Borrowing Stories from Real Americans 🗣️ "I bought my first home using a fully digital mortgage platform — no paper, no agent, just one app. It even suggested the best time to lock in a rate." – Jenna, 29, Colorado 🗣️ "My business got approved for $25K in under 24 hours thanks to POS transaction data. The AI model knew more about my cash flow than I did." – Derrick, 35, Michigan ⚠️ Section 4: The Dark Side of Instant Lending While speed and personalization are great, there's a catch: AI bias can lead to unfair interest rates. Loan stacking from multiple apps can quietly push users into hidden debt traps. BNPL culture is turning short-term borrowing into long-term regret. Data privacy concerns grow as financial institutions use more personal insights. ✅ Section 5: Borrow Smart in 2025 — Pro Tips 📱 Use credit-tracking apps like Credit Karma, Experian Boost, or Chime. 🧾 Read the algorithm’s decision summary — most lenders now provide it. ♻️ Opt for green choices — you'll get better rates and perks. 🤝 Negotiate — just because it’s AI-approved doesn’t mean it can’t be improved. 🔒 Check data-sharing permissions in your banking and fintech apps. 🔮 Conclusion: Borrowing That Works for You “A good loan is not the one that gets approved fast. It's the one that helps you grow without pulling you down.” USA bank loans in 2025 are built around convenience, customization, and connectedness. But behind all the tech, the smartest move is still the most human: stay informed, stay cautious, and borrow with purpose.

.jpg)

💰 Bank Loans in the USA: 2025's Financial Revolution Has Begun

🔍 Section 1: What Makes 2025 Different? 🔹 AI is the New Underwriter Banks now analyze more than just your credit score. They assess: Your earning patterns Lifestyle spending behavior Financial goals Even your career trajectory The result? Loans you qualify for before you even apply. 🔹 Loans with a Conscience Sustainability isn’t just a buzzword — it’s a loan feature. In 2025: Banks offer 0–1% APR for electric vehicles. Home improvement loans prioritize solar and green retrofits. Business loans favor companies with ESG (Environmental, Social, Governance) credentials. 🔹 FinTech + Banking = Embedded Borrowing Need a loan? You may not even realize you’ve taken one. Loans are now: Offered during online checkout. Embedded in ride-share upgrades or tuition payments. Pre-approved and executed via fingerprint or face ID. 🧠 Section 2: Data-Driven Borrower Insights Here’s how different demographics are leveraging this revolution: Demographic Top Loan Types New Benefits in 2025 Millennials Mortgages, auto loans Fast-track approvals, app-based management Gen Z Student & microloans Skill-based repayment plans, financial coaching integration Freelancers Business/personal loans Income pattern recognition, dynamic EMI schedules Green Consumers EV, solar loans Tax credits, eco-incentives, lower rates 💡 Section 3: Real Innovations You Can Use Credit Clarity Dashboards Track your loan status, approval chances, and risk zones in one place. Dynamic Interest Adjustments If your income drops, your rate drops — protecting you from default. Smart Repayment Advisors AI suggests when to pay early, refinance, or consolidate debt for better savings. Risk-Based Loan Shielding Personal loan insurances automatically activate during economic downturns. ⚠️ Section 4: The Hidden Risks The digital-first model is amazing — but not without dangers: Over-personalization = Higher scrutiny. Your coffee habits and phone bill may influence your interest rate. Invisible lending could cause debt stacking — too many small loans at once. Algorithmic bias remains a concern, especially for underserved groups. Data dependency raises ethical and privacy concerns. Always read the fine print. ✅ Section 5: Pro Tips to Win the 2025 Loan Game Know your digital credit trail: Apps like Zogo, NerdWallet, and Chime offer accurate, daily insights. Negotiate terms even if you're approved instantly. AI suggestions aren’t the final word. Choose green, repay less: Federal and bank incentives for sustainable choices are growing every quarter. Bundle smartly: Banks now allow combining personal, business, or educational loans with discounts. 🔮 Section 6: Tomorrow’s Loans (2026 & Beyond) Brace yourself for: Voice-triggered loan requests through home assistants. Credit NFTs for peer-to-peer lending transparency. Emotion-tracked lending: If your wearable detects stress, it pauses loan approvals. Financial Avatars that represent your credit profile in digital space. 🧾 Final Word: The Borrower is Boss "In the new age of banking, power doesn’t belong to lenders — it belongs to the informed borrower." 2025 marks a new chapter in America’s financial story — one written by data, led by transparency, and shaped by personal empowerment. The best way to borrow is to know more, act smarter, and stay one step ahead of the system.

🏦 The New American Credit Era: Inside USA Bank Loans in 2025

🌍 Introduction: Banking in the Age of Personalization In 2025, borrowing in the USA isn’t just about applying for a loan — it’s about how well the system already knows you. From instant approvals to income-linked repayments, bank loans in America have entered a new age — one where personalization, technology, and transparency lead the way. The U.S. financial landscape is now dominated by AI-backed underwriting, climate-conscious credit, embedded lending, and customer-first design. If you’re thinking about borrowing this year — whether to buy a home, start a business, or fund your education — this guide will show you how everything has changed and how you can benefit. 📊 Section 1: The Biggest Changes in 2025 USA Bank Loans 1. AI + Behavioral Lending Models In 2025, banks don’t just look at your credit score. They analyze: Spending behavior Subscription history Freelance/gig payments Mobile app transactions This data feeds predictive models that determine your loan limit, interest rate, and even repayment structure — all in real time. 2. Embedded Lending is Everywhere Loans are now invisible and seamless. While shopping online, buying an appliance, or booking a flight — you’re offered financing at checkout, without needing to visit a bank. 3. Green Loans Get Priority With U.S. banks under pressure to support climate goals, green financing is rising fast: Preferential rates for solar installations, EVs, and sustainable housing. Partnerships with government agencies for eco-incentive loan programs. 4. Dynamic Repayment Systems Borrowers can link their payments to: Freelance income cycles Business profit spikes Tax refund periods This flexibility helps avoid defaults and makes loans feel “lighter” in tight months. 🧑🤝🧑 Section 2: Who’s Benefiting the Most? Borrower Type Loan Benefits in 2025 First-Time Homebuyers AI-prequalified mortgages, digital closings Gig Workers Loans based on app-based income, with seasonal repayment options Small Business Owners Revenue-linked credit, same-day approvals College Students Skill-based student loans with post-graduation grace flexibility Eco-Conscious Borrowers Green auto/home loans with rewards and lower APRs 💡 Section 3: Smart Tech Behind the Scenes Blockchain: Increases transparency in loan terms and contract enforcement. Open Banking APIs: Allows secure sharing of financial data between apps and lenders. Voice & Chatbot Advisors: Guide users in choosing the best loan based on goals. Data Scoring: Alternative credit scoring models use rent, phone bills, and even social trust networks. ⚠️ Section 4: Risks and Red Flags While borrowing has become easier, it’s also riskier if you're not aware: Hidden Fees in BNPL Schemes: "No interest" often turns into backend charges. Over-personalization: Some borrowers face discriminatory rates if their data is misinterpreted. Loan Addiction: Easy credit access can lead to overspending. Privacy Concerns: Your financial patterns are shared — often more widely than you realize. ✅ Section 5: How to Borrow Wisely in 2025 Use AI Budgeting Tools like Copilot, Cleo, or Rocket Money to plan repayments. Check APR and Total Cost — not just monthly payment. Consider Credit Unions & Online Banks for more flexible options. Verify Your Data — request a report of your digital credit profile to ensure accuracy. Explore Government-Backed Loans if you're a student, veteran, or homebuyer. 🔮 Section 6: What’s Coming in 2026? Real-Time Salary-Linked Credit Cards Emotion-Based Credit Assistance (via wearables) Social-Verified Loan Pools — lend and borrow in micro-communities Crypto-Collateral Loans — use digital assets to secure USD-based loans Digital Avatars for loan advice and portfolio simulations 🧠 Final Thought “The new world of lending belongs to those who are financially aware, data-savvy, and digitally equipped.” Bank loans in the USA are now smarter, faster, and more flexible — but they also demand more responsibility. Stay informed, ask the right questions, and use technology not just to borrow — but to borrow better.

💳 Reimagining Credit: How Bank Loans in the USA Are Transforming in 2025

🧬 Section 1: The DNA of a 2025 Bank Loan What makes today’s bank loan radically different from those even five years ago? AI-Powered Risk Profiling: Banks now analyze lifestyle, purchasing behavior, and income volatility to assess creditworthiness beyond the FICO score. Instant Decision Engines: Pre-approved offers and one-click disbursal through mobile apps. Smart Repayment Models: Borrowers can link repayments to their income cycle, profit margins, or even seasonal trends. Eco-Incentives: Opting for electric cars or green homes gets you better interest rates and tax perks. 🧑💻 Section 2: Who’s Borrowing — and Why Here’s how different segments of the American population are leveraging new-age loans: Borrower Type Loan Purpose Key Benefits in 2025 Millennials & Gen Z First-time home & auto buyers Digital-first, zero-paper loans Freelancers Income support or business expansion Flexi-loans tied to online gig income Small Business Owners Equipment, inventory, or cash flow funding POS-linked approvals in 24 hours Sustainable Buyers EVs, solar panels, energy upgrades Green loan incentives, rebates 📱 Section 3: The Rise of Embedded Lending Embedded lending is revolutionizing how Americans borrow. Picture this: You’re on Amazon — and instead of “Add to Cart,” you see “Buy Now, Pay Later – Pre-Approved.” Booking a Tesla? Loan bundled into the checkout flow. Buying a course on Coursera? Get an education loan without leaving the site. This seamless borrowing model is growing across every sector: e-commerce, healthcare, travel, and education. ⚠️ Section 4: Watch Out — Hidden Pitfalls of 2025 Loans Even smart systems can be dangerous if you’re not informed. Risks include: Over-automation: Blindly accepting offers without reviewing terms. Hidden fees in fintech bundles. Surge interest rates triggered by AI predictions of income loss. Predatory BNPL (Buy Now Pay Later) models disguised as “interest-free.” Stay sharp. Not all digital convenience is in your favor. ✅ Section 5: How to Borrow Smarter in 2025 To thrive in this landscape, here’s your action plan: Track your credit health using AI-based apps like Cleo or Tally. Compare more than interest rates — look at APR, duration, and flexibility. Choose lenders with dynamic repayment tools. Leverage your digital history (freelance contracts, gig income, etc.) to negotiate better rates. Explore federal green financing programs that reward eco-friendly choices. 🔮 Section 6: What’s Coming Next? Here’s a glimpse into what 2026 and beyond might look like: Biometric Lending: Authenticate and apply via retina scan or voice. Loan NFTs: Transfer your debt obligation as a token. Emotion-Aware Apps: Get loan recommendations based on financial stress signals. Predictive Saving + Lending Systems: Auto-save to reduce loan dependency altogether. 🧠 Conclusion: Loans That Know You “The best loan isn’t the fastest — it’s the smartest, the fairest, and the one you fully understand.” As America redefines what it means to borrow, knowledge remains your greatest financial asset. In 2025, smart borrowers don’t just accept offers — they control the conversation.

🏛️ USA Bank Loans in 2025: The Age of Intelligent Credit

💡 Key Drivers of the Loan Evolution 1. Hyper-Personalization via Data Intelligence Every click, swipe, and transaction you make is now part of your financial DNA. Banks use this data (securely, with consent) to offer: Pre-approved personal loans Custom interest rates Spending-based repayment plans 2. Climate-Conscious Lending Sustainability is no longer optional. Green loans have surged: 0% interest for EV purchases (with certain banks) Rebates for installing solar energy or insulation Extra credit score rewards for climate-conscious investments 3. Self-Employed and Gig Worker Inclusion Banks now underwrite based on: Platform income (Uber, Upwork, etc.) Digital contracts and transaction consistency AI projections of income stability This opens doors for millions who were once left out of the formal credit system. 🏦 Major Loan Types in 2025 — Reimagined Loan Type What’s New in 2025 Home Loans Digital appraisals, AI-backed affordability assessments Auto Loans EV-first financing, subscription-style vehicle ownership Student Loans Pay-as-you-earn 2.0: Fully dynamic tuition repayment programs Business Loans Pre-qualified based on revenue sync with POS or e-commerce APIs ⚠️ New-Age Borrower Challenges While smarter loans sound attractive, here are hidden risks: Overdependence on auto-approvals: May lead to overborrowing. Algorithmic bias: AI can still misjudge niche income profiles. Digital fatigue: Managing finances entirely online can be overwhelming without education. Privacy trade-offs: Sharing financial data with third parties requires caution. ✅ Smart Borrowing Strategy for 2025 Run your financial profile through multiple apps like Mint, Credit Karma, and your bank’s AI assistant. Compare APR + embedded fees — don’t just look at the interest rate. Go green where possible — banks reward climate-friendly spending. Build a hybrid credit footprint: traditional + alternative (e.g. rent, subscriptions). Use dynamic repayment options that adjust if your income changes. 🔮 The Future of USA Lending — 2026 and Beyond Voice-authorized borrowing via home devices like Alexa. Smart-contract auto-repay via blockchain tied to salary cycles. Emotional AI to detect borrower stress and recommend solutions. Bank-backed financial therapists replacing loan officers. 🧠 Final Thought In 2025, a loan isn’t just a transaction — it’s a tech-driven relationship between your financial habits and your life goals. Whether you’re buying a home, funding your startup, or paying for your child’s education — the way you borrow reflects who you are financially. With knowledge, clarity, and the right tools, you can make that reflection a powerful one.

🏦 USA Bank Loans in 2025: The Digital Transformation of Borrowing

The New Borrower Profile: Who’s Taking Loans in 2025? Tech-Savvy Millennials and Gen Z: Seeking instant approvals and mobile-first experiences. Gig Workers & Freelancers: Demanding flexible payment plans to match irregular income. Small Business Owners: Leveraging digital platforms for quick capital to innovate and scale. Sustainability Advocates: Preferring green loans to support eco-friendly projects and lifestyles. Innovations Shaping the Loan Industry 1. AI-Powered Risk Assessment and Personalized Offers Gone are the days of one-size-fits-all loan terms. AI analyzes transaction histories, employment trends, and even social factors to craft personalized loan offers with competitive rates. 2. Green Loans and Eco-Incentives Banks actively promote loans tied to sustainable projects — like solar panels, electric vehicles, and energy-efficient homes — often offering reduced rates and tax advantages. 3. Income-Adaptive Repayment Models Borrowers with variable incomes benefit from repayment schedules that adjust monthly payments in line with actual earnings, reducing default risk and financial stress. 4. Instant Loan Processing & Disbursement With robust mobile applications and digital identity verification, loan approval and fund disbursement can happen in under an hour. The Role of Cutting-Edge Technology Blockchain: Ensuring transparency, security, and automated contract enforcement. Biometric Security: Fingerprint and facial recognition securing loan accounts. Voice Assistants: Managing loans via conversational AI for convenience and accessibility. Embedded Lending: Seamlessly integrated loans within everyday apps like e-commerce, travel, and ride-sharing platforms.

🏦 Navigating USA Bank Loans in 2025: Trends, Challenges, and Opportunities

Section 1: Who Is Borrowing and Why? Young professionals and first-time buyers are driving demand for affordable mortgages amid fluctuating housing prices. Freelancers and gig workers seek flexible loan structures that accommodate inconsistent income streams. Small business owners require rapid access to capital to adapt and grow in competitive markets. Eco-conscious borrowers prioritize green loans to finance sustainable homes, vehicles, and businesses. Section 2: Key Trends in Bank Loans for 2025 1. AI-Enhanced Credit Assessment Banks leverage AI and machine learning to analyze a broader range of data — including spending habits, employment history, and even social behavior — enabling more accurate risk assessments and customized loan offers. 2. Sustainable and Green Financing Green loans are growing in popularity, incentivizing borrowers with lower rates and rewards for investing in energy-efficient and environmentally friendly projects. 3. Flexible Repayment Solutions Innovative repayment plans adapt monthly installments based on real-time income, reducing default risk especially for those with variable earnings. 4. Instant Loan Approvals Mobile-first applications enable microloan approvals in minutes, providing swift financial relief for urgent needs. Section 3: Technology Driving the Lending Revolution Blockchain and smart contracts increase transparency, automate payments, and minimize fraud. Voice and biometric authentication streamline secure access to loan management. Embedded lending platforms integrate financing options into everyday apps like e-commerce and ride-sharing. AI-powered chatbots assist borrowers with personalized advice and 24/7 support. Section 4: Challenges and Considerations for Borrowers Interest rate fluctuations require careful selection of fixed vs. variable rate loans. Data privacy concerns demand vigilance over how personal data is used. Over-indebtedness risk grows with easier access to credit. Hidden fees and penalties necessitate thorough review before signing. Section 5: Smart Borrowing Tips for 2025 Compare APRs and total costs across lenders. Keep your credit score healthy by managing debts responsibly. Use AI-driven financial tools for budgeting and repayment forecasting. Opt for green loans if eligible to save money and support sustainability. Lock in interest rates amid volatile markets. Section 6: The Road Ahead — Future Lending Innovations AI-driven financial wellness coaching to help borrowers stay on track. Credit products linked to social and environmental impact metrics. Fully integrated platforms combining loans, savings, investments, and insurance. Enhanced security measures with biometric and voice recognition.

🏦 USA Bank Loans in 2025: Unlocking New Opportunities in a Digital Era

Section 1: The Changing Borrower Landscape The modern borrower is diverse: Young adults and first-time homebuyers seek affordable, fast mortgage solutions amid fluctuating housing markets. Gig economy workers and freelancers demand flexible repayment schedules reflecting their irregular incomes. Small and medium enterprises (SMEs) require quick access to capital to sustain and grow their businesses in competitive markets. Eco-conscious consumers are choosing “green loans” that finance sustainable lifestyle investments. Section 2: Innovative Loan Products and Services AI-Driven Personalized Lending Advanced AI models evaluate a wide spectrum of data points — transaction patterns, social behavior, employment stability — to tailor loan offers, reduce default risk, and speed up approvals. Green and Sustainability-Linked Loans Incentives for borrowers investing in renewable energy, electric vehicles, and sustainable housing have become mainstream, offering lower interest rates and tax benefits. Flexible, Income-Responsive Repayment Plans Borrowers with variable income streams benefit from repayment structures that adjust monthly installments based on real-time income verification. Instant Microloans Mobile-first lenders provide small loans approved within minutes, addressing emergency funding needs with minimal paperwork. Section 3: Technology as a Catalyst Seamless digital applications: The entire loan lifecycle from application to funding can be completed on smartphones, cutting down traditional wait times. Blockchain for trust and transparency: Smart contracts automate repayment schedules and reduce fraud. Voice-activated interfaces: Borrowers can manage loans hands-free, from payment reminders to balance inquiries. Embedded lending: Loans are integrated within everyday apps such as e-commerce platforms and ride-sharing, facilitating point-of-need financing. Section 4: Risks & Precautions Rising interest rates may increase monthly obligations — fixed-rate loans are a safer bet. Overborrowing risks are heightened with instant digital access. Data privacy and cybersecurity must be prioritized when choosing lenders. Hidden costs and fees require careful scrutiny before signing agreements. Section 5: Strategic Borrowing Tips for 2025 Shop and compare multiple loan offers beyond just interest rates. Maintain healthy credit scores through timely payments. Use AI-powered financial tools to forecast repayment capabilities. Seek green loans if aligned with your goals. Lock in interest rates when market volatility is high. Section 6: Looking Forward — The Future of Lending AI-powered financial coaching will guide borrowers toward optimal loan management. Lending products will increasingly reward social and environmental responsibility. Financial platforms will unify lending, saving, and investing into a single experience. Voice and biometric security will enhance ease and safety of loan access. Conclusion: Borrow Smarter in a Tech-Driven Economy Bank loans in 2025 offer unparalleled convenience, personalization, and opportunity. However, borrowers must stay informed and cautious to harness these benefits fully. “The future of borrowing isn’t just about credit—it's about leveraging technology and insight to build lasting financial strength.”

🏦 Understanding USA Bank Loans in 2025: Trends, Technology, and Borrower Insights

Who’s Borrowing in 2025? Millennials and Gen Z: Prioritizing homeownership and career development loans. Gig Economy Participants: Seeking flexible loan structures aligned with irregular income. Small Business Innovators: Utilizing fast-track loans to scale operations. Eco-Friendly Borrowers: Opting for green financing with incentives for sustainable choices. Emerging Trends in Bank Loans 1. AI-Enhanced Credit Underwriting Advanced algorithms analyze comprehensive borrower data — including cash flow, spending behavior, and even social metrics — to better predict creditworthiness and customize loan offers. 2. Green Loans and Sustainability Incentives In alignment with national climate goals, many banks offer preferential rates and rebates for investments in renewable energy, electric vehicles, and energy-efficient housing. 3. Income-Adaptive Loan Repayments Loans now often feature adjustable monthly payments based on real-time income verification, reducing default risks and financial stress for variable-income borrowers. 4. Instant Digital Loan Access Borrowers enjoy rapid, end-to-end digital loan processing through mobile apps, with approval times shrinking from days to mere minutes. The Role of Technology in Modern Lending Blockchain and Smart Contracts: Enhancing security and automating disbursements and repayments. Voice & Biometric Authentication: Facilitating seamless and secure access to loan management. Embedded Lending Platforms: Integrating loan options into everyday apps for frictionless borrowing. AI Financial Coaching: Offering personalized advice to help borrowers manage debt effectively. Challenges Borrowers Should Consider Interest rate fluctuations amid economic uncertainty. Risk of overleveraging with easy digital access. Privacy concerns surrounding data-intensive underwriting. Understanding the fine print on fees and penalties. Tips for Borrowers in 2025 Compare APRs, fees, and repayment flexibility across multiple lenders. Maintain good credit by timely payments and low credit utilization. Leverage digital tools and AI advisors to plan and manage repayments. Explore green loan options if eligible. Consider fixed-rate loans in a rising interest rate environment. The Future Outlook Real-time voice-activated loan management. Credit products linked to sustainable and social impact metrics. Fully integrated financial ecosystems combining borrowing, saving, and investing. AI-driven proactive financial health monitoring. Conclusion: Embracing the Future of Borrowing The 2025 bank loan landscape is more accessible, adaptive, and technology-enabled than ever. Borrowers equipped with knowledge and digital tools can navigate this environment to secure the best financial outcomes and build lasting wealth.

💼 The Future of Personal Loans in the USA: What Borrowers Need to Know in 2025

📈 Section 1: Personal Loans by the Numbers (2025) 📊 $235 billion in total outstanding personal loan debt (up 40% from 2020) 📱 80% of personal loans are applied for through mobile-first platforms ⚡ Average approval time: 3 minutes 🤖 65% of loans are approved without human involvement 💡 30% of new borrowers use non-traditional credit data 💡 Section 2: What’s Different About Personal Loans in 2025? ✅ 1. AI Underwriting Is the Norm Instant review of spending, income, job stability Sentiment analysis from your digital footprint (shopping, reviews, payments) Smart risk assessments that adjust loan terms in real time ✅ 2. Non-Credit Score Borrowing You can now qualify based on: Subscription payment history (Netflix, Spotify) Gig work earnings (Uber, Fiverr) Rent payments and digital wallet behavior ✅ 3. Embedded Loans Buy a phone? Add a personal loan with a swipe. Book a flight? Embedded credit offers in booking apps. Need emergency cash? Digital banks now show “pre-approved” overlays based on transaction spikes. 🧾 Section 3: Loan Types Gaining Popularity Loan Type Avg. Amount Popular Among Notable Feature Emergency Loans $1K–$5K Gig workers, students 1-hour disbursal, no credit pull Wellness & Health Loans $2K–$15K Urban professionals Used for mental health, fitness, IVF Subscription Loans $500–$3K Gen Z, freelancers Paid off monthly like Spotify payments Sustainable Living Loans $3K–$10K Eco-conscious citizens Lower APR for green purchases Wedding & Event Loans $5K–$50K Couples, families 0% APR during planning period ⚠️ Section 4: Watch Out for These Risks AI Transparency Gaps Some borrowers are denied without clear explanations — always ask for an underwriting summary. Loan Overlap Auto-approved credit lines can stack without warning — watch your debt-to-income ratio. Hidden Fees in “0% Interest” Plans Some platforms shift costs into item pricing or use short-term interest holidays. Data Trade-Offs You're paying with more than money — always review what data you’re giving up for faster approval. 🧠 Section 5: Pro Tips for Smart Borrowing ✅ Compare rates across digital lenders and neobanks ✅ Read reviews about customer support (post-loan service matters!) ✅ Use loan calculators to understand full repayment amounts ✅ Opt-in for credit education tools bundled with your lender app ✅ Track your “real” affordability — not just what you’re approved for 🔚 Conclusion: A Borrower’s World In 2025, personal loans in the USA are faster, more accessible, and increasingly tailored to the borrower's life. But with great flexibility comes great responsibility. The smartest borrowers will blend convenience with caution, and tech with wisdom. If you’re planning to take out a loan this year, remember: “It’s not just about what you can borrow — it’s about what you can comfortably repay.”

🏦 The Future of Bank Loans in the USA: Trends and Insights for 2025

Introduction: Revolutionizing Borrowing in 2025 In 2025, bank loans in the USA are undergoing a profound transformation. The fusion of technology, data analytics, and shifting borrower needs is reshaping how Americans access and manage credit. Whether you’re aiming to buy your first home, expand a business, or finance education, understanding the evolving loan landscape is essential to making smart, future-proof decisions. Borrower Profiles: Who’s Seeking Loans? Young professionals & first-time buyers: Driving demand for mortgages and personal loans. Freelancers and gig workers: Seeking flexible lending solutions aligned with variable incomes. Small business owners: Prioritizing quick access to capital with minimal friction. Eco-conscious consumers: Favoring green loans with incentives for sustainable investments. Cutting-Edge Loan Products in 2025 AI-Powered Personalized Loans Banks use artificial intelligence to assess creditworthiness beyond traditional scores, factoring in spending habits, employment stability, and even social data to customize rates and terms. Green Loans and Incentives From solar panel installations to electric vehicles, borrowers receive preferential rates and rebates for environmentally responsible purchases. Income-Based Repayment Loans Flexible repayment options adjust monthly payments according to actual income, easing financial stress for fluctuating earners. Microloans for the Gig Economy Short-term, small-value loans provide liquidity to freelancers and contractors, often approved instantly via mobile apps. Technology’s Role in Lending Instant approvals via mobile platforms: Streamlined applications reduce wait times dramatically. Blockchain for transparency: Smart contracts secure loan agreements and automate payments. Voice-activated loan management: Borrowers monitor and control loans hands-free through smart assistants. Embedded lending: Loans integrated into apps like e-commerce, ride-sharing, and freelancing platforms for seamless access. Risks and How to Navigate Them Interest rate fluctuations: Lock fixed rates where possible to avoid surprises. Overborrowing: Maintain awareness of total debt load and avoid stacking loans. Data privacy: Use lenders with strong cybersecurity measures. Hidden fees: Read loan terms carefully to uncover origination fees, prepayment penalties, and other costs. Smart Tips for Borrowers in 2025 Shop around: Compare APRs and full loan terms. Keep your credit healthy: Timely payments and low utilization remain key. Leverage digital tools: Use budgeting and AI advisory apps to plan repayments. Understand green incentives: Explore loans that reward sustainable investments. Stay informed: Keep up with market trends and Fed policies that affect borrowing costs. Looking Ahead: The Next Frontier in Lending AI financial coaches: Personalized real-time advice to optimize borrowing. Sustainability-linked credit products: Rates tied to eco-friendly behaviors. Voice and biometric authentication: Faster, secure loan processing. Integrated financial ecosystems: Borrowing, saving, and investing managed in one app. Conclusion: Borrowing Smarter for a Secure Future The landscape of bank loans in the USA in 2025 is more dynamic, personalized, and technology-driven than ever. Borrowers who embrace innovation, remain vigilant, and plan strategically can unlock unprecedented opportunities for growth and financial resilience.

🏦 Navigating the New Era of Bank Loans in the USA: What Borrowers Must Know in 2025

Who’s Borrowing and Why? A Snapshot of 2025 Borrowers Young Professionals & Entrepreneurs: Seeking startup capital, personal growth, and home ownership. Gig and Remote Workers: Demanding flexible, income-sensitive loan products. Eco-conscious Consumers: Opting for green loans with incentives for sustainable purchases. Small Business Owners: Leveraging data-backed loans for faster capital access. Common loan uses include: Mortgage and refinancing (42%) Education and skill development (18%) Vehicle financing, especially EVs (15%) Business expansion (13%) Medical and emergency expenses (12%) Innovations in Bank Loan Products and Processes AI-Driven Credit Assessment Gone are one-size-fits-all credit decisions. Banks now use AI to evaluate diverse data—employment history, spending patterns, digital behavior—to offer tailored interest rates and credit limits. Eco-Friendly Loan Options Green mortgages and auto loans reward borrowers who invest in energy efficiency and carbon reduction with lower rates and rebates. Flexible Repayment Plans Income-based repayments, subscription-style loans, and pause-pay features address volatility in borrower income streams. Fully Digital, Instant Approvals End-to-end loan applications happen on smartphones, with decisions in minutes, using blockchain for transparency and security. Integrated Financial Wellness Tools Loan providers now bundle coaching, budgeting apps, and alerts to help borrowers manage debt sustainably. Key Challenges Borrowers Face Interest Rate Uncertainty: Rising Fed rates can increase borrowing costs quickly. Debt Overextension: Easy credit can tempt over-borrowing. Data Privacy Concerns: Sharing personal data requires trust and safeguards. Complex Loan Terms: Hidden fees and confusing contracts demand borrower vigilance. Best Practices for Borrowers in 2025 Understand APR & Total Loan Costs: Look beyond headline rates to all fees and terms. Maintain Healthy Credit Scores: Timely payments and low credit utilization remain vital. Compare Multiple Lenders: Fintech, credit unions, and traditional banks all compete for your business. Use Tech Tools: Apps and AI advisors can model scenarios and warn against risky borrowing. Plan Repayments Strategically: Avoid stacking loans and consider fixed-rate options when possible. The Future of Borrowing: What to Expect Voice-Activated Loan Management: Approve loans and manage payments hands-free. Embedded Lending Experiences: Loan offers appear in everyday apps—shopping, ride-hailing, freelancing. Sustainability-Linked Credit: Borrowers rewarded for reducing carbon footprints and social impact. AI-Powered Personalized Coaching: Proactive advice to optimize borrowing and financial health. Conclusion: Empowered Borrowing for a Brighter Financial Future Bank loans in 2025 are more than just money—they’re strategic tools shaped by innovation, flexibility, and social responsibility. Borrowers who stay informed, use technology wisely, and plan carefully will unlock not only funds but also opportunities for lasting financial well-being. “In a rapidly evolving economy, smart borrowing isn’t just about credit—it’s about clarity, control, and confidence.”

💳 Unlocking Opportunities: The Evolution of Bank Loans in the USA, 2025 Edition

Section 1: The Changing Face of Borrowers Millennials and Gen Z dominate borrowing: Nearly 60% of new loan applications come from borrowers under 40. Gig economy impact: 25% of loan seekers now rely on freelance income streams. Small business surge: Post-pandemic entrepreneurship has led to a 15% year-over-year increase in small business loan demand. Diverse loan purposes: Housing (40%), education/skills training (20%), business expansion (18%), healthcare (12%), and vehicle financing (10%). Section 2: Cutting-Edge Loan Products in 2025 Green Home Loans Designed for energy-efficient and sustainable homes, these loans offer reduced rates, rebates, and extended terms for properties meeting strict environmental standards. AI-Enhanced Personal Loans Banks leverage machine learning to evaluate creditworthiness holistically—beyond FICO scores—considering employment patterns, digital footprint, and cash flow for tailored rates. Income-Responsive Student Loans Flexible repayment plans tie monthly payments directly to borrower income, reducing default risk and financial stress. EV Auto Financing Loans with integrated carbon credits and maintenance bundles incentivize electric vehicle adoption, coupled with buyback guarantees. Microloans for the Gig Worker Short-term, small-dollar loans help freelancers manage cash flow gaps, often with instant approvals through app integrations. Section 3: Technology Driving Loan Accessibility Instant Digital Approvals: AI-driven underwriting can approve loans in under 5 minutes. Mobile-First Applications: 85% of loans initiated via smartphone apps. Blockchain Smart Contracts: Enhancing transparency and speeding up disbursement. Personalized Loan Offers: Dynamic interest rates adjusted in real-time based on borrower behavior. Section 4: Risks and How to Mitigate Them While opportunities abound, risks persist: Rising Interest Rates: Borrowers should hedge against variable rates by locking fixed rates when possible. Data Security: Protect your personal info; use banks with strong cybersecurity. Loan Stacking: Avoid borrowing from multiple lenders simultaneously to prevent debt traps. Understanding Terms: Always review all fees—origination, prepayment penalties, and late charges. Section 5: How to Borrow Smartly in 2025 Analyze the Total Cost: Use online calculators to understand your total payment over the loan term. Maintain Good Credit Hygiene: Pay bills on time and keep credit utilization low. Leverage Financial Tools: Budgeting apps and AI advisors can optimize repayment schedules. Ask About Incentives: Green loans, loyalty discounts, and bundled services can save money. Section 6: The Future Outlook Voice-Activated Lending: Manage loans via Alexa, Google Assistant. Embedded Lending Ecosystems: Loan offers directly within shopping, ride-share, and freelancer apps. Sustainability-Linked Loans: Rates tied to borrower’s carbon footprint reduction progress. AI Financial Coaches: Real-time advice to avoid over-borrowing and optimize repayment.

💵 Bank Loans in America 2025: Navigating New Frontiers of Borrowing

The Borrower of 2025: Who’s Taking Out Loans and Why? Millennials and Gen Z: Leading the demand for personal and business loans, often through digital-first platforms. Gig Economy Participants: Freelancers and contractors require flexible loan options tailored to irregular income. First-time Homebuyers: Thanks to rising real estate prices, many rely on specialized loans and grants. Small Business Owners: Looking for fast, data-driven financing options to keep up with a competitive market. Top Reasons for Borrowing: Homeownership and refinancing Education and skill upgrades Vehicle purchases, especially electric vehicles Medical bills and emergency expenses Business growth and innovation Innovations Shaping Bank Loans Today 1. AI-Powered Loan Underwriting Banks increasingly use AI algorithms analyzing not just credit scores, but spending habits, employment stability, and social signals, delivering personalized interest rates and faster approvals. 2. Green Financing Loans incentivizing eco-friendly investments — like solar panels or energy-efficient appliances — offer lower rates and tax benefits. 3. Subscription Student Loans A new wave of student loans lets borrowers pay monthly fees only after landing a job, easing upfront financial strain. 4. Integrated Digital Applications From application to approval, the entire loan journey is mobile-first and paperless, allowing approval in minutes. 5. Hybrid Loan Products Combining traditional bank loans with fintech features like flexible repayments, loyalty rewards, or bundled services (insurance, financial coaching). Risks and Considerations While loans are powerful tools, pitfalls remain: Variable Interest Rates: Can increase unexpectedly, especially on personal and business loans. Hidden Fees: Origination fees, prepayment penalties, and deferred interest can increase costs. Over-leveraging: Taking on multiple loans without a clear repayment strategy. Data Privacy: Increased data collection raises concerns about personal information security. Smart Borrowing Tips for 2025 Always compare the Annual Percentage Rate (APR), not just interest rates. Keep your debt-to-income ratio below 35%. Utilize digital financial tools to simulate repayments before borrowing. Read the fine print carefully to avoid surprise fees. Choose lenders who prioritize transparency and data security. What’s Next for Bank Loans? Voice-Activated Loan Services: Apply and manage loans using smart home devices. Blockchain Contracts: Secure, transparent loan agreements with instant verification. Embedded Lending: Loan offers integrated directly into apps like ride-sharing or e-commerce platforms. AI Financial Advisors: Personalized loan advice and monitoring in real-time. Social Impact Lending: Loans tied to sustainability goals and community development. Conclusion: Empower Your Financial Future Bank loans will continue to be critical tools for personal growth and economic development. But with rapidly evolving technology and market conditions, educated, strategic borrowing is more important than ever. Remember: A loan is more than money — it’s a commitment between your present and future self. Borrow wisely, plan carefully, and watch your dreams become reality.

💸 The Future of Bank Loans in the USA: What Borrowers Need to Know in 2025

Who’s Borrowing and Why? The Modern Borrower Profile: Age 25-40: Millennials and Gen Z leading the charge in personal and business loans. Gig Economy Workers: Freelancers and contractors seeking flexible financing. First-time Homebuyers: Representing nearly 40% of mortgage applications. Small Business Owners: Launching and scaling with tailored SBA and alternative loans. Loan Purposes: Home purchases & refinancing Education and career development Medical and emergency expenses Business growth and innovation Auto purchases, especially electric vehicles Types of Bank Loans Dominating 2025 1. Green Mortgages Banks incentivize eco-friendly homes with lower rates and perks — from solar panels to energy-efficient appliances. 2. AI-Underwritten Personal Loans Artificial intelligence evaluates your financial habits and spending behavior, offering customized interest rates beyond traditional credit scores. 3. Subscription-Based Student Loans Innovative models let students “lease” education and pay back only when employed — easing upfront financial burdens. 4. EV Auto Loans Loans for electric vehicles come bundled with maintenance and insurance offers, sometimes tied to carbon footprint rewards. 5. Digital Business Loans Tailored for startups and gig workers, with rapid approvals based on real-time revenue data rather than historic credit alone. Key Trends Shaping Bank Loans Faster Approvals: Digital-first lenders approve loans in minutes. More Transparency: Clearer disclosure of fees, thanks to new federal regulations. Data Privacy Concerns: Borrowers more cautious about sharing behavioral data. Increased Competition: Neobanks and fintechs pushing traditional banks to innovate. Interest Rate Volatility: Borrowers need to watch for changing rates tied to Fed policy. How to Borrow Wisely in 2025 Understand Your APR: Don’t just look at the interest rate; factor in all fees. Keep Debt-to-Income Ratio Low: Aim below 35% to maintain good credit health. Shop Around: Compare offers from banks, credit unions, and fintech lenders. Avoid Over-borrowing: Borrow only what you need with a clear repayment plan. Leverage Financial Tools: Use apps to simulate loans and track payments. The Road Ahead: What’s Next? Voice-Activated Loan Applications: Imagine applying for loans through smart assistants. Blockchain-Verified Lending: Secure, transparent loan contracts powered by distributed ledgers. Lending Embedded in Everyday Apps: From shopping to ride-sharing, get loan offers contextually. AI-Powered Financial Coaching: Real-time advice to avoid debt traps. Social Impact Loans: Loans tied to sustainability and community development metrics. Conclusion: Borrowing as a Strategic Tool Bank loans remain vital to American dreams, but their power depends on how you use them. In 2025, smarter borrowing means blending traditional wisdom with new tech insights. Approach loans not as last-resort fixes, but as strategic tools to build lasting wealth and opportunity. “The best loan is the one that propels you forward — financially and personally.”

💰🇺🇸 Borrowed Dreams: How Bank Loans Are Reshaping American Lives in 2025

🧾 Section 1: The Modern American Borrower — Profile of 2025 📍 Key Demographics: Average borrower age: 34 Top loan purposes: Home ownership (38%) Business expansion (21%) Medical expenses (14%) Debt consolidation (12%) Credit score average: 683 (FICO) 📲 Digital Lending Has Taken Over: 74% of bank loans are now fully digital, with no in-person visits AI now reviews 90% of applications before a human ever sees them Average time to approval: 6.2 minutes 💳 Section 2: Top Types of Bank Loans in the U.S. 🏠 Mortgage Loans Still the largest loan segment. In 2025: First-time buyers under age 30 make up 41% Federal Smart Home Grants reduce rates if your house has solar panels or energy-efficient cooling 🧰 Personal Loans Used for: Home renovations Credit card consolidation Weddings, emergencies, and even IVF Rates: 8.9% – 15.4% Term: 2–7 years 🚗 Auto Loans EV car loans dominate — with embedded Tesla/GM partnerships inside bank apps Flexible repayments based on driving behavior and carbon offset usage 🎓 Education Loans Now include VR/AI skill certifications and bootcamp financing Subscription-based student loans (pay monthly after employment) are gaining traction 💼 Small Business Loans $3.2 billion disbursed in the first quarter of 2025 Special programs for: Women entrepreneurs Veterans Gig economy startups (Etsy sellers, digital freelancers, food trucks) 🧠 Section 3: The Psychology of Loans in 2025 Loans today aren't just about "can I afford this?", but also "can I grow from this?" Americans now view loans as: Launchpads (to buy, build, expand) Bridges (between paychecks or job changes) Safety nets (in a high-cost healthcare economy) But with this empowerment comes a risk: normalizing debt as progress, without a clear repayment strategy. 🧨 Section 4: Common Traps in 2025 Lending Even as systems get smarter, borrowers fall into new traps: ❗ Trap 😟 Hidden Consequence Buy-now-pay-later overdoses Credit score crash, unexpected fees App-based loan stacking Multiple microloans = compound stress Variable-rate personal loans Jump from 8% to 22% in under 18 months Early repayment fees Punishes good behavior 💡 Section 5: How to Borrow Smarter in 2025 ✅ Check APR, not just rate ✅ Compare 3 lenders, especially one digital-only bank ✅ Avoid interest-only plans unless it's temporary ✅ Use tools like Plaid or Mint to simulate debt impact ✅ Always read the data usage agreement—your loan behavior is now monetized

🏛️💬 Bank Loans in 2025: A Deep Dive into the Backbone of the American Economy

🏦 Section 1: The Current State of Bank Lending in the USA 📊 Lending Snapshot (as of June 2025): Total outstanding U.S. consumer debt: $17.1 trillion Average mortgage rate: 6.5% (fixed) Average personal loan interest: 11.3% Fastest-growing segment: Gig-worker microloans & digital business capital 🔄 Lending is now: Faster: Approvals within minutes using AI Smarter: Creditworthiness scored by your behavior Riskier: More approvals = more defaults, especially with flexible lending apps “What used to take 7 days now takes 7 minutes—but the consequences still last 7 years.” 🧠 Section 2: The Psychology Behind Modern Borrowing In today’s digital world, a loan isn’t just a contract—it’s a relationship with time. You borrow for what you want now and pay with what you hope to earn later. People borrow not just because they’re broke, but because: Credit feels empowering Delayed gratification feels outdated Spending is easier than saving But that freedom has a flip side. Americans are facing rising delinquencies in auto and personal loans, and over-leveraging is silently growing. 🔍 Section 3: New Age Loan Types You Need to Know 🏡 1. Eco-Conscious Mortgages For homes with solar, smart insulation, or net-zero design Lower interest + green tax credits 🚘 2. EV Auto Loans Extended terms up to 96 months Bundled with insurance + carbon offset tokens 🎓 3. Subscription-Based Student Financing No upfront tuition Monthly "knowledge lease" paid post-employment 📈 4. Creator Loans For YouTubers, influencers, and digital entrepreneurs Based on subscriber count, brand deals, or AdSense income 🔐 Section 4: Behind the Scenes — What Banks Are Really Analyzing Forget just your credit score. In 2025, banks also factor in: ✅ Factor 🔍 Why It Matters Real-time income stream Are you earning consistently? App usage habits Are you a risk-taker or a planner? Location & spending clusters Are you living within or above means? Digital behavior signals Do you impulse spend or save smartly? Data is the new down payment. 📉 Section 5: Hidden Pitfalls Most Borrowers Miss Even in 2025, fine print kills more dreams than bad credit. Deferred interest traps: “0% for 12 months” flips to 24% after Origination fees: Up to 5% on personal loans Early repayment penalties: Especially on business or debt restructuring loans Credit stacking: Multiple small loans = one giant repayment sinkhole 🔎 Always read the Annual Percentage Rate (APR), not just the interest. APR = interest + all fees. 💡 Section 6: Smarter Borrowing Strategies Want to borrow like the top 10%? Use these modern rules: Borrow for value creation (home, business, education), not consumption Track your Debt-to-Income ratio — Keep it under 35% Use a loan only when the return exceeds the rate Consolidate smartly — Avoid juggling 5 lenders Protect your privacy — Use secure portals & opt out of data-sharing when possible 📈 Section 7: Where Loans Are Headed Next 🔮 Predictions for 2026 & Beyond: Voice-enabled lending via smart assistants Blockchain-verified personal loan agreements AI underwriters with no human intervention Global credit passports — your history follows you across borders Banking APIs inside social media — imagine loan offers on your Instagram feed 🧾 Final Word: Borrow With a Plan, Not Just a Need Bank loans aren't bad. They’re tools. Just like a hammer builds homes or destroys walls, a loan can build your future—or break your finances. In 2025, being loan smart is a survival skill. “Before you sign, ask: Is this funding my future—or financing my fear?”

🧠💸 The Psychology of Borrowing: Why Americans Take Bank Loans — And What It Really Costs in 2025

🏛️ Part 1: America’s Debt Culture — A Love-Hate Relationship In 2025, the average American carries $92,850 in debt. From student loans to business capital, borrowing isn’t just a financial action—it’s a cultural habit, a coping mechanism, and sometimes, a silent act of survival. Banks are no longer dusty buildings on Main Street. They’re smartphone apps, AI bots, and invisible algorithms. But while the face of borrowing has changed, the emotions remain the same: hope, fear, pressure, ambition. 💳 Part 2: Types of Loans—More Than Just Money Bank loans aren’t one-size-fits-all. Each one tells a different story: 🏠 Mortgage Loans — “The American Dream Loan” Rate (2025): ~6.3% fixed | 5.9% adjustable Term: 15–30 years Trend: First-time homebuyer programs now offer climate incentives (solar credits, insulation rebates). 🚗 Auto Loans — “Wheels for the Future” EV-specific loans now come with federal discounts and free charging station vouchers. Max term: 96 months Many banks link your vehicle’s GPS to risk scoring—drive safer, pay less. 🧰 Personal Loans — “Financial Glue” Used for: Weddings, IVF, medical debt, travel, side hustles Up to $100,000 unsecured Fast disbursal: under 24 hours for qualified borrowers 🧑🎓 Student Loans — “Hope in a Contract” Federal loans fixed at 5.5% Private loans as high as 12% In 2025, borrowers can now “subscribe to education”—pay monthly instead of upfront (Income Share Agreements are booming again). 💼 Business Loans — “Capital Meets Courage” SBA loans up to $5M Gig-based loans (for Uber drivers, Etsy sellers, freelancers) have surged by 33% YoY 🔍 Part 3: The New Loan Approval Formula in 2025 In a traditional bank, you needed: Credit score Income proof Collateral In 2025, you might also be evaluated on: AI-driven digital footprints Spending behavior analytics Browser cookies and app usage Real-time payroll API access Privacy vs Access: Want fast money? Trade your data. 🧠 Part 4: Why We Borrow — The Hidden Psychology Americans don’t just borrow because they need money—they borrow because of: Social pressure: Weddings, kids, college, cars—everything’s a benchmark. Survival: 62% of borrowers in 2024 cited medical bills or inflation as the reason. Entrepreneurial ambition: Over 5 million Americans took loans in 2024 to start small businesses. “Debt feels heavy—but freedom sometimes costs interest.” 🔥 Part 5: Loan Risks Most People Ignore Even with tech upgrades, dangers still lurk: ❗ Risk 💥 Consequence Variable rates Sudden 3x monthly payments Early repayment penalties Unexpected fees Hidden origination fees Loss of upfront capital Data misuse Algorithmic denial in future Modern tip: Always check for the APR, not just interest rate. APR includes all fees. 📈 Part 6: Top Borrowing Trends of 2025 Embedded Loans: Buy a phone, get a bank loan in-app in seconds. Crypto-Collateral Loans: Stake Bitcoin to borrow USD. Eco-Scoring: Borrowers get better rates if their purchases align with sustainability goals. 💡 Part 7: Smart Borrowing Checklist ✅ Compare at least 3 lenders (traditional + fintech) ✅ Know your Debt-to-Income ratio (aim < 35%) ✅ Use loan simulators for worst-case scenarios ✅ Keep a repayment buffer (at least 3 EMIs in savings) ✅ Protect your data with secure loan portals only 🧭 Conclusion: Borrow Boldly, Not Blindly Bank loans are neither good nor bad. They’re a financial tool—like a scalpel in a surgeon’s hand. In 2025, where AI makes the decisions and your data tells the story, the smartest borrowers are the ones who ask the right questions, not just the lowest rates. If you’re planning to borrow this year, don’t just get a loan—get educated.

🏦🇺🇸 Bank Loans in the USA: What You Need to Know Before Borrowing in 2025

🏛️ Section 1: The Core Types of Bank Loans in 2025 1. Home Loans (Mortgages) Typical Rate: 6.25%–7.10% (fixed), 5.85% for adjustable Loan Terms: 15 to 30 years Down Payment: 5%–20% New FHA programs are making it easier for first-time homebuyers to enter the market, especially in affordable housing zones. 2. Auto Loans Terms: 36–84 months Rates: 5.5%–10% depending on credit EV Loans: Extra 1% discount offered by green-focused banks Electric and hybrid vehicles are now eligible for extended loan durations of up to 96 months at subsidized rates. 3. Personal Loans Unsecured, ranging from $1,000–$50,000 Rates: 7%–20% Used for: Medical bills, travel, home improvements, debt consolidation Many banks are integrating AI to offer pre-approval decisions within minutes, even for unsecured lending. 4. Student Loans Federal interest: Fixed at 5.5% (2025–2026 cycle) Private loans: Range from 6.5%–12% APR Income-driven repayment plans remain available for federal loans, and many banks now offer private education loan refinancing. 5. Small Business Loans SBA 7(a) loans and microloans remain popular. Amounts: Up to $5 million Terms: 10–25 years Rates: ~6.75%–9% depending on type and credit history Digital banks like Bluevine and Fundera are offering faster SBA-backed loans with lower documentation requirements. 📉 Section 2: How Borrowing Behavior Has Changed In 2025, Americans are borrowing less frequently but more strategically: Many Gen Z borrowers avoid long-term loans, preferring flexible or buy-now-pay-later (BNPL) financing. Debt consolidation loans are in high demand due to rising credit card interest (now averaging ~22% APR). Gig workers and freelancers are applying for income-based loans with bank partners that support non-traditional employment. 🔍 Section 3: What Lenders Look For Today To improve approval chances in 2025, banks are focused on: ✅ Credit score (700+ for prime rates) ✅ Debt-to-Income Ratio (preferably under 36%) ✅ Verified income with tax returns or real-time payroll API access ✅ Stable banking behavior (no recent overdrafts or late fees) Tip: Tools like Plaid and Experian Boost are helping consumers improve their credit profiles automatically. 📲 Section 4: The Rise of Digital Lending More than 72% of bank loans in 2025 are initiated or completed online. Key Features: AI-powered approvals within 5–15 minutes eSignature & remote KYC Instant disbursal via direct deposit Neobanks (like SoFi, Chime, and Ally) now compete aggressively with traditional banks by offering cashback on loan payments or free financial coaching. ⚠️ Section 5: Common Pitfalls to Avoid Even with automation, many borrowers fall into traps: Variable rate confusion: Rates that adjust every 6 months may look low today but rise later. Hidden origination fees: Some banks charge 1%–5% just to process the loan. Over-borrowing: Many borrowers take the maximum amount offered, not the minimum needed. Pro Tip: Use online comparison platforms like NerdWallet, Bankrate, and Credit Karma to shop for the best deal. 📈 Section 6: 2025 Lending Trends to Watch Credit Inclusion: More banks are lending to immigrants, gig workers, and low-credit-score applicants with alternative credit data. Embedded Finance: Banks are integrating loans directly into e-commerce apps (buy furniture, get loan instantly). Federal Regulations: A national Personal Data Protection Act (PDPA) is under review, which may restrict how banks use consumer data for loan profiling. 🏁 Conclusion: Borrow Wisely, Plan Ahead Bank loans can unlock opportunities—but only when used responsibly. In the dynamic 2025 lending environment, borrowers must stay informed, compare their options, and understand the long-term financial impact of their choices. 💡 Whether it’s for a new home, car, education, or business—know before you owe.

🏦 USA Bank Loans in 2025: Deep Dive into Trends, Risks, and Borrowing Strategies

Introduction: Understanding the Evolving Dynamics of Bank Loans in the United States In 2025, the landscape of bank loans in the USA is undergoing profound transformations fueled by technological advances, economic fluctuations, and evolving regulatory frameworks. For borrowers—from individuals to small businesses—successfully navigating this complex environment requires a nuanced understanding of current trends, inherent risks, and best practices. This article explores the key dimensions of bank lending today and offers strategic guidance to optimize borrowing outcomes. 1. Technology-Driven Disruption in Lending Artificial Intelligence & Machine Learning Banks leverage AI-powered algorithms that assess creditworthiness using both traditional financial data and alternative signals such as: Employment stability trends Utility and rental payment histories Real-time cash flow monitoring This approach improves risk prediction accuracy but also introduces challenges related to fairness, explainability, and borrower trust. Digital Loan Origination and Automation Digital-first platforms streamline loan applications with features including: Instant eligibility checks Automated document verification E-signature capabilities The result: faster approvals, reduced paperwork, and expanded access for underbanked populations. Blockchain and Smart Contracts Emerging blockchain applications enable secure, immutable loan agreements and automate repayment processes through smart contracts, increasing transparency and efficiency in loan servicing. 2. Regulatory Landscape & Consumer Protection Regulatory bodies including the Consumer Financial Protection Bureau (CFPB) and state agencies are enforcing stricter oversight over digital lenders to: Ensure transparency in loan terms and fees Protect consumers from predatory lending and discriminatory practices Mandate data privacy compliance aligned with laws such as the California Consumer Privacy Act (CCPA) Borrowers should stay informed about these protections and their rights. 3. Overview of Popular Loan Products and Innovations Loan Product Recent Innovations Primary Borrowers Personal Loans Flexible repayment, AI-driven interest rates Consumers with variable income sources Mortgages Green incentives, digital closing processes First-time buyers, environmentally conscious homeowners Auto Loans EV financing, telematics-based risk pricing Buyers of electric and hybrid vehicles Business Loans Hybrid fintech-bank models, revenue-based repayments SMEs, startups seeking flexible capital 4. Key Risks and Challenges for Borrowers Data Privacy Risks: Expanded data collection increases vulnerability to cyber threats and misuse. Algorithmic Bias: AI lending models may inadvertently discriminate against minorities or low-income applicants. Overborrowing: Easy access to credit can encourage unsustainable debt accumulation, especially amid inflationary pressures. Economic Instability: Rising interest rates and market fluctuations can tighten credit availability and increase borrowing costs. 5. Strategic Tips for Borrowers in 2025 Maintain Strong Credit Health: Regularly monitor your credit reports, dispute inaccuracies, and manage debt levels. Use Comparison Tools: Employ fintech platforms to shop and compare loan offers efficiently. Understand Loan Terms: Scrutinize interest rates, fees, and repayment schedules before committing. Negotiate When Possible: Lenders may offer better terms based on your creditworthiness and relationship history. Seek Professional Advice: For complex borrowing needs, consult financial advisors or credit counselors. 6. Future Outlook: What Lies Ahead for U.S. Bank Lending Looking forward, the banking sector is expected to embrace: Open Banking Ecosystems: Enabling secure data sharing and personalized credit products. Ethical AI Frameworks: Ensuring transparency, fairness, and accountability in lending decisions. Blockchain Adoption: Streamlining loan origination and servicing with immutable records. Sustainability-Focused Lending: Increased incentives for green and socially responsible borrowing. Conclusion Navigating the U.S. bank loan market in 2025 demands a keen understanding of emerging technologies, regulatory safeguards, and economic conditions. Borrowers who stay informed, leverage digital tools wisely, and adopt disciplined financial habits will be well positioned to access credit that supports their financial ambitions safely and efficiently.

💼 Economic Change in the USA: What’s Shaping Our Financial Future?